Our year

to tatou tau

All previous reports can be found at moana.co.nz

Tēnā koutou katoa

2024 is a significant moment in our business as we acknowledge 20 years since formation, and we honour our whakapapa by recognising Māori rights to fisheries through Te Tiriti o Waitangi.

It’s timely to acknowledge all those who were part of the Settlement negotiations, two of whom, Tā Tipene O’Regan and Whaimutu Dewes, went on to serve as Moana Chair. It is their legacy, and others, we carry forward and continue to serve.

There have been some movements within the Moana Board this past year. I would like to extend my deep appreciation for departing Moana director Rangimarie Hunia’s strong leadership within Māori fisheries and welcome Dean Moana and Bella Takiari-Brame to the Moana Board. Bella is a seasoned director, is our Te Ohu Kaimoana representative to the Moana Board, and is a Chartered Member of the Institute of Directors and a Fellow Chartered Accountant of Chartered Accountants Australia and New Zealand. Dean has a long career in the kaimoana industry and is an experienced director with present directorships including the Iwi Collective Partnership, Akaroa Salmon, and Ngati Porou Seafoods.

I’m pleased also to welcome two new associate directors Emma Winiata and Cornell Tukiri. I look forward to their fresh insights and contributions as we share our knowledge from leadership and governance perspectives.

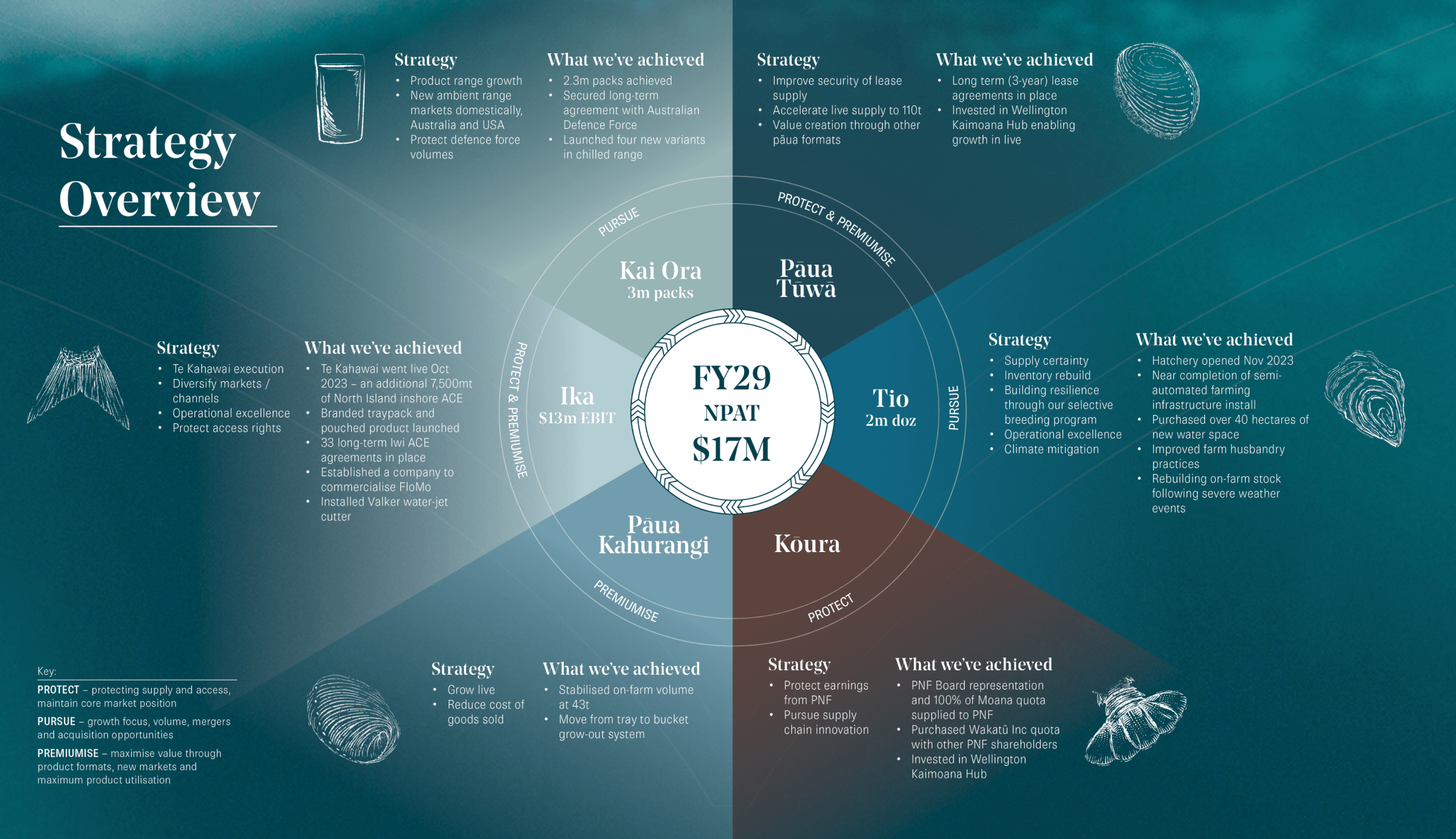

We each bear significant responsibility in caring for the taonga entrusted to us through the Fisheries Settlement on behalf of all Iwi. I am incredibly proud of our achievements, our team, and their mahi through the year. Despite headwinds of the last two years we have completed and opened our Kaimoana Hub, invested in Sealord such that they might acquire IFL, and through our Sanford deal we have become the largest inshore seafood company in the motu. As we continue to build on the strong foundations created by those before us, I’m pleased to share some insights into our current strategy and accomplishments from the past few years.

This year the Moana Board of Directors is declaring a dividend of $6.58 million for the 2023/2024 financial year. More detail around this result is outlined in the CEO report and financial highlights.

As Chair of the Moana Board, I’m incredibly pleased to take time this year to reflect on our past and embed ourselves in the mahi we do now to carry the momentum we’ve built together for our future.

Ngā mihi nui.

Resilience has been a key theme for our business for the last several years and 2024 is no different, so it's pleasing our operating earnings before tax and interest of $12.4 million was an improvement of $1.5 million or 13% on the 2023 result.

In our half-year report, we commented that as a consequence of entering into the long-term lease of Sanford's Inshore North Island quota the International Financial Reporting Standards (IFRS) would require the recognition of a significant right of use (ROU) asset and corresponding lease liability. The impact of this accounting standard was adverse to our reported earnings after tax for the first four years of the lease and, conversely, beneficial in the last four years. After considering further advice that identified an alternative treatment using the short term leases exemption, we are now amortising the annual cash cost of the Sanford lease on a similar basis to other annual catch entitlement (ACE) leases. The revised accounting treatment benefits the 2024 earnings by $2.6 million.

Overall, Ika harvest volumes were down 12% on Plan, but up 58% on 2023 catch. While access to the Sanford ACE was delayed by one month the more critical delay was access to two additional trawlers, which did not come online until February 2024. This delay meant a change in catch plans and focus for the rest of the fleet which ultimately contributed to 12% lower than plan catch with sales volumes down by a similar magnitude. On a positive note, operating costs were nearly 8% under Plan which is due to a combination of the lower throughput volumes as well as lower than expected incremental costs arising from taking on the Sanford ACE volumes.

Our Pāua Tūwā me te Kai Ora earnings were 33% down on Plan and 20% down on 2023 earnings. While the contribution from Kai Ora was above Plan expectations due to product mix, the key driver of underperformance against both Plan and last year was canned Pāua Tūwā, which historically has been a mainstay of our business. Demand and pricing have been under pressure all year in our key markets of Singapore, Malaysia and Hong Kong due to a combination of cost-of-living pressures, and pricing pressure and reduced demand caused by Chinese canned abalone gaining increasing consumer acceptance.

While Tio recorded a loss of $1.3 million, this was $2.5 million better than Plan and an improvement on the 2023 result by $1.8 million. As reported last year significant weather events in the first half of calendar 2023 resulted in a stock loss of just under 50% and given the 18-to-24-month life cycle the rebuild of our farm biomass will continue through into 2025. Total sales volume was on Plan although average pricing was down 3% due to sizing. The lower than Plan loss is mainly due to much lower operating costs than Plan on the back of increased wild supply.

Earnings from Pāua Kahurangi, our farmed pāua operation based in Ruakākā, were on Plan although down on 2023 earnings. Similar to live Pāua Tūwā, demand and pricing in China came under pressure in the second half of the year and the adverse impact was offset by lower operating costs.

Kōura earnings through the Port Nicholson Fisheries (PNF) partnership exceeded our Plan by 10% and were slightly up on 2023 earnings. With over 95% of catch sold live to China and commanding the number one spot compared to lobster from other parts of the world the profit extracted from this species is directly correlated to the buying behaviour of wealthy consumers in China. While demand and pricing were solid in the first half of 2024 there was a weakening in the second half as unfavourable economic conditions in China started to dampen demand – leading PNF to hold back catch for the first half of the new lobster fishing season which commenced on 1 April 2024.

As discussed more fully below, our 50% share of Sealord’s earnings is a profit of $26.8 million which is a significant improvement on the 2023 loss of $2.0 million. Note however that the 2024 earnings include our share of a non-cash, net one-off gain of $14.8 million. Putting that aside, our share of the normalised Sealord earnings, which include earnings arising from 1 February 2024 following the acquisition of IFL, is still a significant improvement from last year.

Our total bank interest expense for the year of $6.3 million was higher than Plan by $1.5 million and $2.3 million higher than 2023. The approved 2024 Plan did not include any contribution towards Sealord’s financing of the purchase of Independent Fisheries Limited (IFL). In late January 2024, we injected $20 million into Sealord for that purpose – the unplanned interest cost associated with funding this injection was $1.1 million.

I would like to acknowledge Moana's very loyal and supportive customers and shareholders whose ongoing support is a key component to our success. The other plank to that success is the Moana "secret sauce" being our incredible kaimahi, contract fishers, farmers and divers. Without all of their hard mahi, passion and dedication there is no achieving our result - they are the heart and soul of our business.

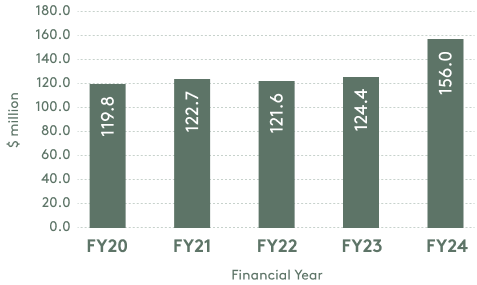

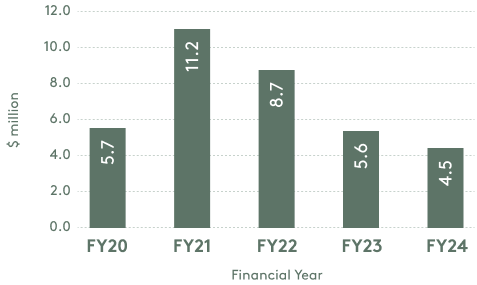

Product FOB Revenue has been relatively stable for the last four years with a significant jump in FY24 due to the additional Ika ACE now leased from Sanford.

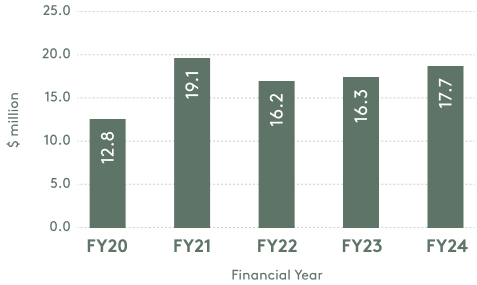

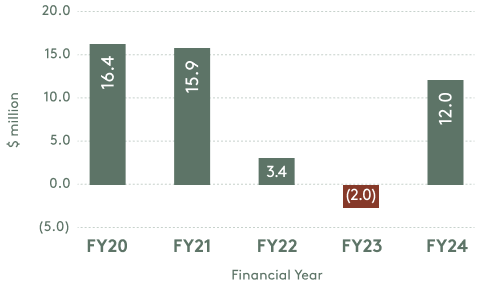

While Moana EBITDA showed a significant increase from FY20 to FY21 due to impact of COVID on kōura earnings, the increase in the FY24 headline number is due to additional Ika ACE now leased from Sanford and recovery from the weather-related events that impacted Tio earnings in FY23.

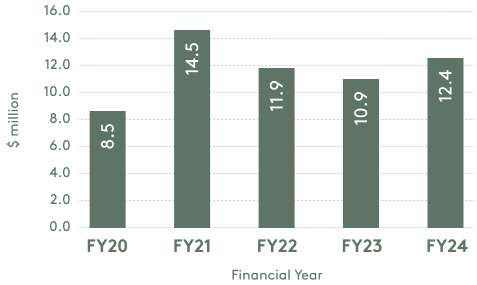

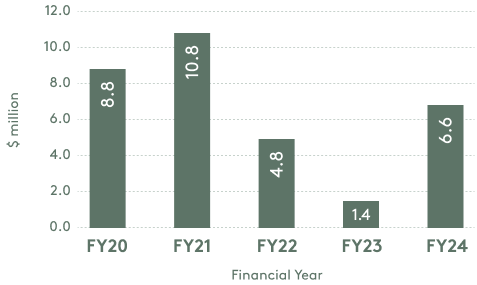

Factors similar to EBITDA have affected EBIT headline earnings although the depreciation cost has increased from $4.3 million in FY20 to $5.6 million in FY24 due mainly to capital expenditure for the Tio Transformation Project.

The improvement in EBIT has been eroded by a significant increase in finance expenses due to a combination of increasing interest rates and higher levels of debt, including a $20 million equity injection in January 2024 to assist Sealord fund the acquisition of IFL.

Our 50% share of Sealord earnings had a significant decrease in FY22 and FY23 with a bounce back in FY24 (the FY24 earnings above exclude the impact of non-cash net one-off items, but includes the net benefit of operating earnings arising from the acquisition of IFL).

The net earnings from Moana’s own business activities and 50% share of Sealord’s earnings (adjusted for the non-cash net one-off items in FY24) is paid out to shareholders at the statutory rate of 40% (fully imputed).

For specie-specific highlights, go to our downloadable 2024 Annual Integrated Report.

This year, Moana delivered its fifth group-wide employee engagement survey. We measure the engagement of our people using periodic, confidential surveys that provide us with a meaningful assessment of employee motivations, their likelihood to remain with Moana, their ability to do their best work every day, and whether they would recommend Moana as an employer.

Feedback is shared with leaders and employees, with action plans co-created within teams to improve ways of working and culture. Since the 2022 survey, this has led to several improvements, including the introduction of an Executive Leadership Development programme, enhanced employee benefits such as paid birthday leave and health insurance, and a new training framework Learn@Moana.

Our employee engagement score for FY24 was 65%, which is above the ANZ median for companies and a 15% increase from our 2022 result. We saw valuable changes in our people's understanding and connection with our whakapapa and values.

Our People & Culture team continues to support senior leaders and managers by providing resources, standards, and guidelines to help them hire talented candidates with diversity in mind. This year, we prioritised hiring frontline roles to support operations, particularly with the establishment of a night shift team in our Mount Wellington, Auckland processing facility.

The prestigious Global Fisheries Scholarship programme, established in 2004 in partnership with Nissui Corporation, continues to deliver a programme to talented rangatahi, reflecting our shared commitment to cultivating talent and nurturing the capability of tomorrow's leaders. This year, we awarded two deserving recipients, Adair Houia-Ashwell and Daria Bell, who will take up the scholarship in 2025 and 2026, respectively. Both recipients are committed to developing their careers in the fisheries sector in Aotearoa and possess the skills and talent to be exceptional Māori business leaders of tomorrow.

As Moana looks ahead to opportunities and challenges, we are focused on resetting our standards for leadership and building environments where people thrive.

We launched the inaugural Leadership Survey this year as a prelude to the Leadership Forum held in November. With 100% participation in the first cohort, the survey provided a comprehensive assessment of leadership confidence, capability in giving and receiving feedback, understanding of management responsibilities, and personal development areas. The insights and feedback from the survey were integral to designing the two-day forum and have acted as a pulse check for assessing engagement levels and the success of programmes introduced last year.

As a Māori-owned organisation, we are committed to equity and ensuring our training helps everyone. Our training modules are designed to invest in developing the whole self of our people, enabling them to focus on personal development, how they work with others, and creating meaningful moments for people participating in workshops and the workplace.

This year, three new training modules were introduced to the Group Employee Training Framework, with 10 foundational modules now offered to support the advancement and acceleration of skills and knowledge building with our kaimahi. Our plan for 2025 is to explore how we can work with new and existing partners to enhance our training community and strengthen our training offering.

We introduced mandatory employee training in 2023, with all employees required to complete a Workplace Respect module as part of their induction into Moana. This foundational training supports the growth of a healthy work environment, focusing on our people's mental and social wellbeing and embedding our collective way of working, led by our values.

We take a purpose-led approach to improving and delivering our diversity and inclusion practices and ambitions. We are committed to building a business for future generations and ensuring all our people have a greater understanding of who we are, which allows us to create experiences and provide support tailored to the diverse needs of our people while staying true to our whakapapa.

In August 2024 we reached a milestone with our health and safety reporting and registered the 10,000th entry in our health and safety management system – The Tackle Box.

Over 75% of those events were lead indicators such as great catches, hazards, and observations by our team. That’s thousands of observations our kaimahi search for, see, and report on each year. What looks good, what we can improve on across the motu for the overall safety of every one of us.

We continue to maintain our focus on what could cause serious injury or fatality (SIF). Having information from our observations helps us put our efforts into becoming a learning organisation. We learn and take positive steps on the path of continuous improvement.

Over the past year our learnings have resulted in continuous improvement in critical risk areas of man/machine interface and guarding, and some of those improvement opportunities were because of the 550+ critical risk observations.

With a full stop on FY24 the following year will see the business continuing our focus on prevention and embedding the culture to lead, learn and manage our critical risks to keep our workers safe at Moana New Zealand.

It was a transitional year for Ika, as we adapted to the increased volumes across our supply chain from the long-term lease agreement with Sanford for their inshore ACE.

Overall, our harvest volumes were 88% of Plan, which contributed to lower sales volumes reflected in our full year EBIT contribution of $7.1 million.

Free on board sales revenue (NZD selling price less export freight) was $102 million from 11,274mt green weight equivalent, which was 90% of Plan. This is compared with $68 million from 7,450mt green weight equivalent for the same period last year, highlighting the increased volume throughputs.

Demand has been under pressure for much of the year primarily driven by the cost-of-living crisis in Aotearoa. Despite this, our domestic market channels continued to show their resilience making up 67% of total green weight sales volumes, and while export channels remained soft, our sales team collaborated with current customers and identified new ones to build ongoing demand moving forward.

Development of the new Kaimoana Hub in Porirua, Wellington, was a significant project and milestone completed in September this year. This site consolidates our Wellington-based Ika and Pāua Tūwā operations as well as Kōura in collaboration with our Port Nicholson Fisheries partner.

Our Ika team fully transitioned its operation to the new facility in October 2024 along with Pāua Tūwā and Kōura management and administration functions. Our swimming and export packing activities remain at the Rongotai facility until China listing registration is completed, which is anticipated before the end of the calendar year. This consolidation of business operations will provide us with significant opportunities for more integrated operating efficiencies across the businesses over the coming years.

The last 12 months has provided many new learnings for the team that have and will benefit us moving forward, however, our focus remains on consistently delivering on forecast catch volumes, continuing to improve production and operational efficiencies across our supply chain and better understanding customer and market requirements to support delivery of our 2025 Plan.

Kai Ora (ready-to-eat meals) revenues met Plan. Revenue from military meals exceeded Plan by 8%

Better than Plan performance from the Australian Defence Force volumes was offset by the New Zealand Defence Force component falling short of Plan by 11%.

Moana New Zealand was ultimately unsuccessful in achieving listings for the chilled Kai Ora range with Woolworth’s New Zealand, leaving retail domestic retailers 40% short of Plan for the year.

Harvest was slower for the first half of the year but lifted to push Pāua Tūwā live sales to year-end resulting in 357mt landed, which was 94% of Plan.

The slower demand for canned volumes has meant an increased requirement to maximise live sales. This has required the team to focus harvesting in key areas where increased live quality product could be sourced with planning around increased swimming capacity and team capability also being implemented to support delivery of the necessary switch in format.

In the first half of the year, we experienced difficulty in securing volume amidst recessive economic conditions in key Asian canned pāua markets and with an increase in both quantity and quality of Chinese canned abalone at significantly lower pricing. Several Hong Kong-based buyers have reduced their retail footprint and closed 30-50% of their retail stores. In Malaysia, our foodservice offer experienced significant replacement with lower-priced Chinese products.

Efforts to secure volume through the second half came with a 20% price reduction in Singapore. Hong Kong buyers reported carry over stock from a slow Chinese New Year and have remained reluctant to purchase and add to those stocks since March.

The harvest team delivered on an ambitious Live volume on Plan despite occasional weather induced gaps. In contrast to lower canned demand for Chinese New Year, Live was in demand for the same period in China at premium pricing. However, late season pricing was adversely impacted by Australian live, green-lip abalone volumes offered at levels below New Zealand pricing, prompting even loyal buyers to consider a switch. While we have strived to retain volume, it has been at the expense of pricing previously secured.

The result from low first half volume and low second half pricing was a full year result $2.6 million short of Plan EBIT due mainly to the lower canned product margin. We continue to explore alternative, value-added product streams to offset lower canned demand should that continue as economic conditions improve.

Our Kōura earnings are generated through our partnership with Port Nicholson Fisheries, a pan-Iwi business solely focused on the Kōura supply chain and live exports to China.

Kōura FY24 earnings are above Plan by $1.2 million or 10%. The full year result reflects Moana’s share of PNF’s profit for the second half of the 23/24 lobster season and first half of the 24/25 season in addition to 12 months of the fixed quota return.

Our share of PNF’s profit was $0.8 million higher than our 2024 Plan. The quota return was also $0.3m higher than our Plan due to the increased quota rates set by PNF for the new season commencing 1 April 2024.

Despite the outstanding result, trading conditions have been difficult particularly in the second half of our financial year with soft and fragile demand resulting in lower-than-expected pricing.

While most fishery management areas (FMAs) performed well, CRA3 (East Coast/Mahia) catch rates continued to struggle with nearly 50% of the ACE available to PNF remaining uncaught at season end 31 March 2024. Following a consultation process, from 1 April 2024 the TACC for CRA3 was cut by 20%, which increased to 30% by industry voluntarily shelving a further 10% to promote a faster recovery of the fishery.

The formal re-entry of Australian lobster has finally been announced and although the exact timing is unclear it is reported that the sanctions would be lifted in time for the 2025 Chinese New Year. Australian lobster has been banned since October 2020 and its formal re-entry will undoubtedly have an impact on pricing for PNF.

Although full year revenue for Pāua Kahurangi fell 5% short of F24 Plan, average pricing was ahead of Plan

by 3.5%.

Late season export pricing and demand was made more difficult by other exporting nations lowering their prices, but higher export pricing earlier in the season and lower than Plan air-freight costs supported the full year price average. Sales were consistent, but not as strong as the previous financial year.

Domestic demand and pricing remained firm throughout the year and as a result, achieved 11% higher revenues than Plan, supporting the average price improvement.

On farm, Project Stabilise (implemented in 2021) has proven successful in maintaining harvest volume and holding farm costs steady. Over this past financial year, the absence of extreme water temperature fluctuations meant less electricity was used to cool water, which allowed pāua to grow continuously through summer months with less mortalities. Management at the Ruakākā site has also been successful in holding costs steady.

Pāua mince has been launched in the domestic market over the past few years and presents an opportunity within our domestic sales channels.

While Tio recorded a loss of $1.3 million, this was $2.5 million better than Plan and an improvement on the 2023 result by $1.8 million.

Due to the flow on effect of the 2023 weather events and the impact on the growth of last year’s juvenile stock into this year’s mature stock, we have strived to ensure allocations of lower than planned volumes to highest priced market alternatives. This has meant that Australian frozen half-shell experienced lower export volumes than Plan, but the domestic chilled market has seen consequently higher allocations due to the higher pricing available on larger chilled half-shell grades. Smaller grade oysters performed well with cruise industry customer demand recovering from the downturn throughout and after Covid.

FY24 was a significant year for Sealord. With the support of Moana and Nissui, they acquired Christchurch-based Independent Fisheries Limited (IFL) on 31 January 2024, making them the largest seafood company in Aotearoa.

IFL holds the fourth largest New Zealand deep-sea fishing quota package, with the consolidated Sealord Group now the largest quota holder in the motu. The purchase of IFL is also the largest financial transaction in the seafood sector since the Sealord deal in 1992 as part of the Māori Fisheries Settlement. All IFL quota purchased is held within the Pupuri Taonga Trust together with all of Sealord’s existing New Zealand quota, ensuring ownership in perpetuity for iwi. The IFL purchase further affirms iwi as major players in New Zealand’s seafood industry.

Together with 46,000 tonnes of quota, the IFL purchase includes two owned and one chartered deep sea fishing vessels, 500 crew and land-based staff and a modern cold storage facility in Christchurch. Eight months into Sealord ownership, IFL has proven to be an excellent fit, and sales, operating and cost synergies have been above those expected in the business case.

FY24 also saw the successful completion of the comprehensive Enterprise Resource Planning (ERP) system replacement at the beginning of the year. In the second half of the year, Sealord also wound down our King Reef barramundi business in Northern Queensland, with completion of the final asset sales on 29 November 2024.

At Sealord Group level, the Net Profit After Tax (NPAT) result is a profit of NZD 53.6 million. This result includes two material one-off non-cash items. The largest is a “bargain purchase” gain on the acquisition of IFL’s quota, with independent quota valuations required under NZ IFRS 3 Business Combinations concluding that the fair value of the quota acquired is higher than the purchase price. Partly offsetting this is the P&L impairment of the King Reef barramundi assets and associated foreign currency translation reserve. After adjusting for these items, NPAT was 23.9 million, and the proposed FY24 Sealord dividend will be based on 40% of this number.

It is pleasing to see all three of Sealord’s operating divisions hit their profit targets in FY24. This included the core Sealord fishing business returning to profitability and IFL meeting its acquisition plan number despite a second poor squid season in a row. Sealord is looking forward to their first full year of IFL operations in FY25, including further optimising their portfolio of deep-sea fishing assets and associated operations.

The Petuna business in Tasmania enjoyed a second successive record EBIT year, with local market pricing remaining strong for these species and our recent expansion investments at the Rowella grow-out farm and Cressy hatchery also supporting the results.

We are pleased with the strategic decisions made and executed during FY24, and a focus on further integrating and simplifying Sealord’s deep-sea fishing operations in FY25 to grow the underlying NPAT for shareholders.

The theme of the last two years has been the fight against inflation and a global economic downturn. While there is still downward pressure, Moana's strong foundation puts us in a good position to realise benefits

from improving economies.

External factors such as two major international conflicts (Ukraine and the Middle East), a potential tightening in US trade policy, and the economic performance of Aotearoa’s largest trading partner (China) all contribute to an uncertain economic outlook. We anticipate demand being soft across most of our sales channels in the short term, which will limit our ability to increase prices to recoup some of the significant cost increases absorbed during this period.

For Ika the increased TACC for most snapper areas provides opportunity for volume growth, including the potential increased catch of inshore trawl mix species in FMA8 (North Island West Coast) in particular. However, the key challenge for snapper will be to find suitable new customers outside of the domestic and Australian markets which are already at capacity. Moving into our second year of operating with access to the Sanford North Island inshore ACE, including having the requisite fishing capacity from day one, will also deliver further benefits as operating efficiencies are realised.

Tio is expected to further recover over 2025 as we rebuild our on-farm stocks after the significant weather-related mortality events of 2023. We expect to sell nearly one million dozen over 2025 which is nearly 70% more than sold in 2024.

Market conditions for Pāua Tūwā will be challenging due to both the state of the Chinese domestic economy where demand is weak (our target market for live pāua tūwā) as well as demand for canned pāua tūwā in Singapore/Malaysia/

Hong Kong where substitution from Chinese farmed abalone is increasing and placing pressure on both order volumes and pricing.

While the re-entry of direct export of Australian lobster to China has been announced, the timing of that change is uncertain but likely to be in time for the Chinese New Year festivities. While in reality most of that volume is likely to already be reaching China through the grey channel, it is anticipated that the formal re-entry will have an adverse impact on the price realised by PNF. In addition, demand in general has been subdued in recent months due to the same reasons noted above for our live pāua tūwā.

Pāua Kahurangi has been in a stable operating position for the last three years although growth prospects (other than price realisation) are minimal. We do not expect this to change over the next 12 months although, again, note that pricing of even the small volumes that we export live to China is currently under pressure.

Operations map

Moana New Zealand uses an online portal Orchestra, which is available for shareholders to access all dividend statements and communications relating to the dividend. Only authorised email accounts have access to the folder holding the dividend statements for their organisation.